Property strategies

Property is generally a very good investment option. It can provide you with a monthly income, as long as the income is greater than your outgoings. Long-term, provided you buy at the right time in the property cycle, you could expect to see the value of your property and investment increase.

As you start to learn about property investment, the more overwhelming it can feel. The good news is that there are many different strategies you can follow to make money from property. Before you start searching Rightmove for an investment opportunity it is important that you have a strategy in mind. A strategy is a bit like a business plan. Without one you can’t recognise your goals or assess the risks you’ll be making. Even with a thoroughly researched opportunity, in an area where property values are set to rise and the perfect purchase price – there is always risk.

Here we’ve written about some of the most popular strategies, from residential buy-to-lets to HMOs. We’ve included some pros and cons to consider, ideas of timeframes and money needed in your investment project.

To help you visualise how tasty some of these strategies are we’ll be using cake (who doesn’t love cake?!?). Read on to find out if you are more of a Victoria sponge cake or a Millionaire Shortbread kind of investor!

BTL (Buy to let)

Buy to let (BTL) is the most popular strategy for those investing in property in the UK. It is the simplest strategy and easy to get up and running but that doesn’t make it dull. Your Victoria sponge cake. Easy recipe to follow, tasty in the centre and you can add extra toppings. There are many variations of the BTL strategy and you don’t need to follow just one. Just find the one that works for you.

A ‘traditional’ buy-to-let: renting out your property as a single element to a professional individual, couple or family. Location is a key ingredient for your success as you’ll have a better chance of finding a good tenant, ensuring a steady rental income – gaining short term benefit and if the area is up-and-coming, positive capital growth should follow – rewarding you in the long term. Unless you are buying your property in cash, you’ll need at least a 25% deposit to get started. If your property needs refurbishing then you’ll need money for this too. It’s likely that your funds will be tied up in the property until you can add value and can refinance.

As with any strategy it’s important to get your numbers right – we’ll be writing a blog soon running through the calculations spreadsheet we use.

Pros and cons of the BTL strategy

| Pros | Cons |

|---|---|

|

|

Commercial

Commercial property investment strategy is fundamentally the same as your residential BTL, but with a business as your tenants instead. A lemon drizzle. An easy recipe like your sponge except with a zesty twist on top. The strategy involves buying a commercial or retail property but you won’t need to spend out on redecoration or furnishing. They also require less ongoing work. Leases and lets tend to be on a much longer basis, often multiple years. Plus if you let on a fully repairing and insuring basis, you’ll save money on insurance and maintenance.

Commercial properties are subject to the whims of the economy. Many high streets have been shrinking and closing down with commercial buildings being left empty. Location and the type of business you have as tenants are key. If you lose a tenant it can take a long time to find a new one, meaning you may be facing long void periods.

One of the more popular ways to diversify with a commercial property is to buy a shop with a flat above and to let out the shop to a business and the flat to a tenant. With this strategy you should see a constant rental yield from the commercial property, and it should also appreciate if you buy it in the right area.

Pros and cons of the Commercial strategy

| Pros | Cons |

|---|---|

|

|

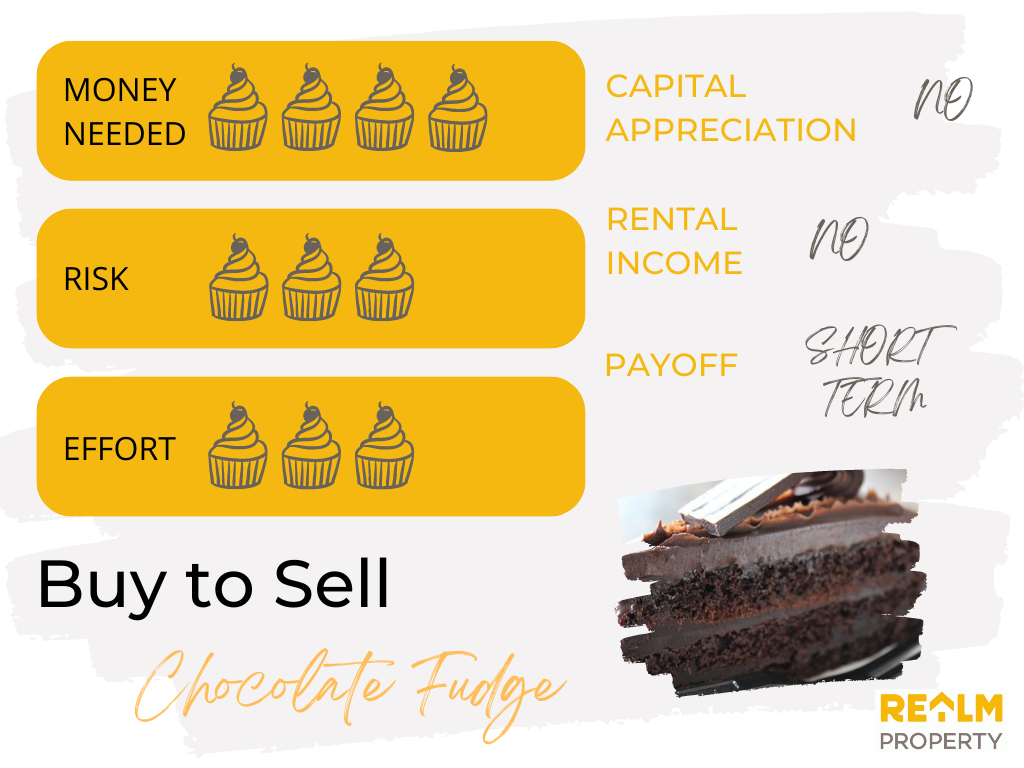

Buy to sell (“flipping”)

The buy-to-sell strategy, more commonly known as ‘flipping’ is simply buying a property, giving it a makeover and selling it on for a profit. The focus is entirely on making short term gains and quickly. Your chocolate fudge cake. Easy to make, though your ingredients are a bit more expensive. Made right you will be in for a gooey, chocolatey delight. A successful flip could make you thousands of pounds in a few months, whereas a buy-to-let property might make a couple of hundreds of pounds per month. But you’ll get your money back in one hit, there is no regular monthly income.

Buying the property below market value (BMV), very likely in need of work and in the right location are the two ingredients for this recipe to work. We’ve all avidly watched ‘Homes under the Hammer’ and started searching on Rightmove for a suitable property that could generate us enough profit to retire early on. However it’s a very demanding strategy. The work can be challenging, expensive and time consuming depending on if you are doing the work yourself or taking on a contractor.

Effective budget management is vital and you want as quick a turnaround as possible. Unless you are planning to live in the property whilst you’re carrying out the work, you won’t be able to mortgage it. Many investors often use short term finance such as a bridging loan to pay for the property and the refurbishment. These can carry reasonably high interest rates so you don’t want to be left on them for too long.

Pros and cons of Flipping a property

| Pros | Cons |

|---|---|

|

|

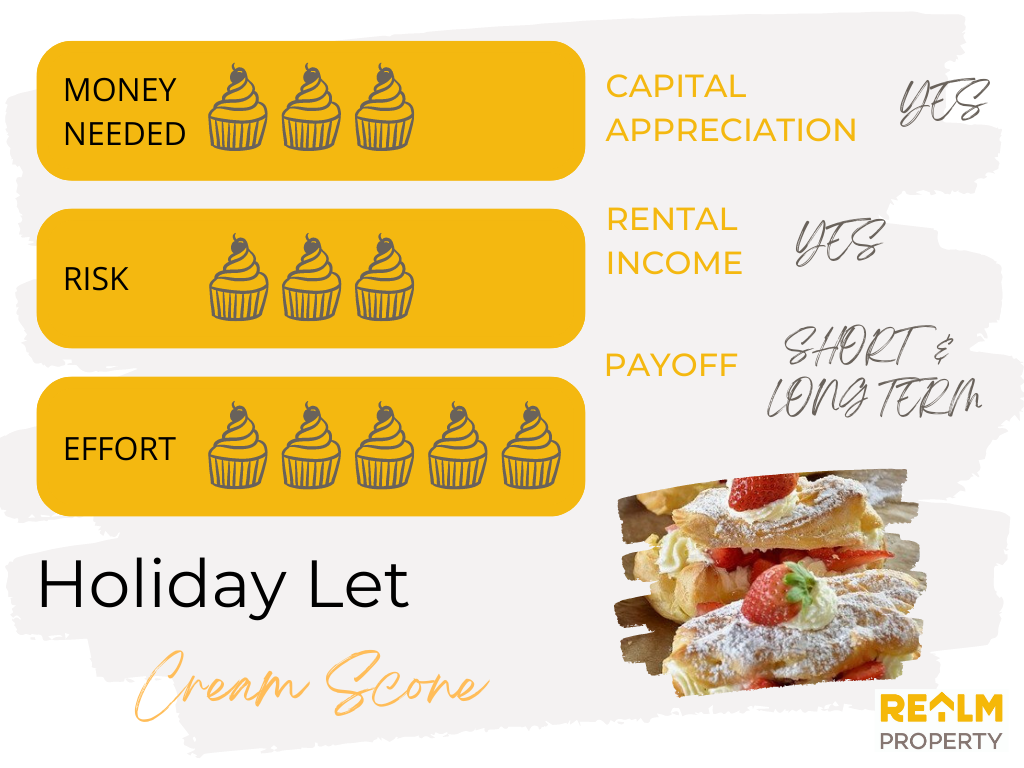

Holiday let or serviced accommodation

The serviced accommodation (SA) property strategy is a relatively new one and might appeal to some investors as it can deliver excellent rental returns. Unlike a single BTL, with serviced accommodation you essentially let a property out to ‘guests’ rather than tenants on a short-term basis. Usually, by the night or at least a short period of time. Typically serviced accommodation is targeted towards business travellers. Holiday letting is the same approach but you are aiming at holiday makers instead.

Prime location is the main factor is a successful holiday let or serviced accommodation property. If the local area draws in holiday makers or has multiple corporate businesses nearby then you will be able to achieve a high level of occupancy all year round. Not just during the summer months. A week’s holiday income could easily exceed that received from a monthly BTL rate. Much like your cream scone. The inside is filled to the brim with sweet jam and thick, rich cream much like the profit you could make. On top you can dress it up to look extra fancy and appealing with fresh strawberries and maybe even some chocolate. Ensuring that it catches your holiday maker’s eye.

Purchasing a holiday let property is similar to that of a BTL. You will need to have the money to refurbish your property and fully furnish it – down to the kitchen utensils. Guests expectations are higher and comparable to staying at a hotel, so if your property is finished to a high standard then it is likely to attract more bookings. Mortgage providers are now beginning to offer serviced accommodation or holiday let products. These are typically higher rates than those of a BTL and you need to ensure that your insurance covers short term stays. Often your insurance premium will be higher as they consider short stays are likely to carry a greater risk.

Managing a serviced accommodation or holiday let property is very labour intensive. There are frequent change overs of guests, bookings to manage and being on hand when your guests are staying if they have any issues. There are property management agencies that can take care of all your bookings, cleaning, linen etc but they will take around 20-25% fee off your booking. With so many people coming and going, maintenance is going to be high and frequent. Any damage needs to be repaired or replaced quickly, ideally before the next guests arrive. You will be charging a higher nightly rate compared to that of a BTL but its also worth noting that you will be responsible for paying all bills including utilities, wifi and TV subscription.

Pros and cons of a Holiday Let strategy

| Pros | Cons |

|---|---|

|

|

HMO or House of multiple occupancy strategy

A HMO (house of multiple occupancy) is where a property is rented out by room to individual, unrelated tenants. Basically a house share. This strategy means you’ll likely be purchasing an existing HMO, or you’ll need to convert a property to make it suitable. The idea of this strategy is that you can increase your rental return by renting each room for more than you can by renting the entire property as a whole. The more rooms your HMO has, or has the ability to have, the more income you can gain.

Like with most things there are layers of complexity to be aware of. Which is why the HMO strategy is a Millionaire Shortbread.

In large towns and cities there is often a demand for affordable housing with flexible living for different types of tenants. HMOs can work for people from social housing, to students, to professionals. By renting a room it makes it more affordable for the tenant but they can still enjoy a larger space within the house.

Purchasing an existing HMO is not likely to come cheap. If you do manage to find one on the market at a reasonable price then it’s probably going to need some modernisation. You’ll also need extra funds to refurbish and furnish to a high level. In particular, professionals looking to rent a room in an HMO are demanding a higher standard of finish. There can be further expense if you choose to include bills within the monthly rent, offering an all-inclusive package. Owning an HMO also comes with more complicated tax rules, planning regulations and legislation requirements. A licence is required if a property is occupied by 5 or more people. The local council authority may also have additional licensing or requirements too.

Managing a HMO requires a great deal of time. Having a number of tenants all under one roof can, not surprisingly, cause tensions. There may be times you’ll need to step in to mediate certain situations. Typically you will see a higher turnover of tenants in an HMO which means regularly advertising the rooms, doing viewings, vetting the tenants etc. With more people living in the property than a single let it is common for there to be more wear and tear, breakages etc. If you’ve furnished the property then as landlord you’ll need to repair or replace most items.

Pros and cons of a HMO

| Pros | Cons |

|---|---|

|

|

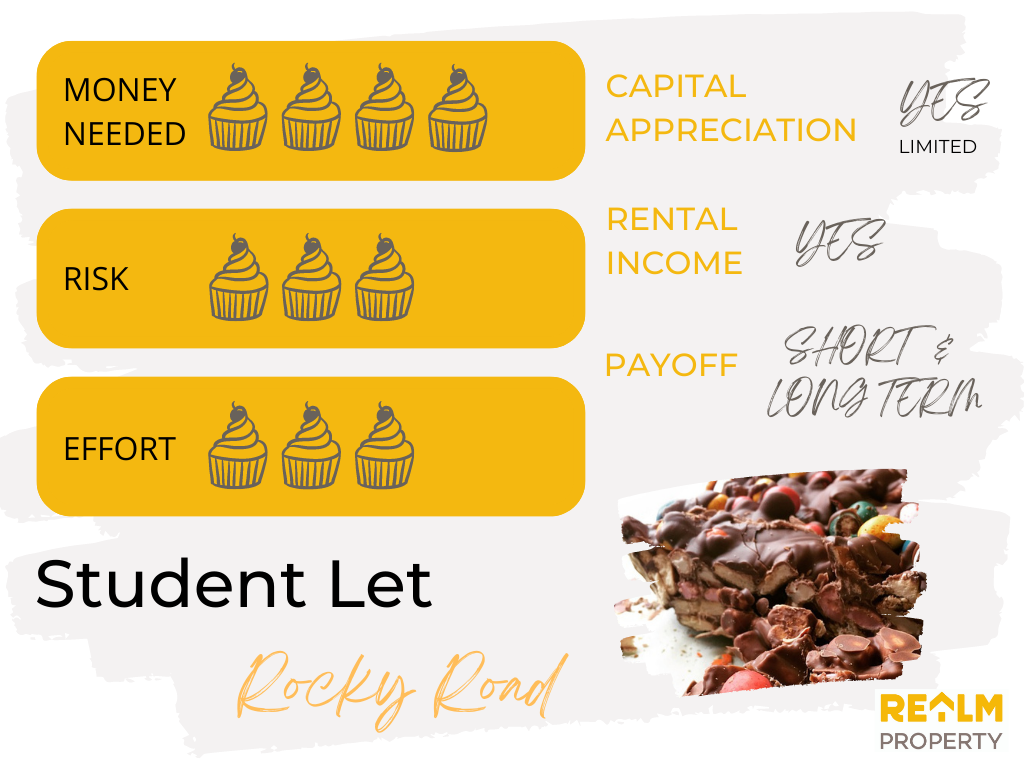

Student let

In many ways a student let is very similar to the HMO strategy. Typically you’ll purchase a house or flat and rent it out to multiple student occupants. Obviously the location of your property is key. It needs to be accessible to local amenities, the university buildings and everything else a student will want to reach. Unlikely to have a car a student will probably rely on local transport, walking or possibly the occasional Uber. A Rocky Road. Combining a mixture of tasty ingredients, smothering them in chocolate and putting in the fridge to set.

There is less expectation of furnishing to a high standard and more basic than that of an HMO. So less money would be required to refurbish the property. However this is changing due to the competition from new purpose built student accommodations. All inclusive packages where bills are included are becoming increasingly popular too.

Student tenants are possibly slightly less volatile than an HMO as it may be that some tenants are friends already. Typically because of the seasonality of the student market you will secure one joint tenancy agreement for the property, meaning that if one of them leaves the remaining tenants will have to continue paying their share of the rent.

| Pros | Cons |

|---|---|

|

|

Realm Property Investment are still actively pursuing opportunities. We are out actively viewing properties and will pay good referral fees for any opportunities that go through to purchase.

We offer great returns on your investment but without the hassle. Get in touch if you would like to learn more. To read more about our recent projects head to our projects page.